Developing economies need trillions of dollars to meet climate goals, yet many still face financing costs more than twice those in advanced markets.

By Ankush Kumar

As the cost of solar panels, wind turbines, and battery storage continues to fall, one barrier to decarbonization remains stubbornly high: the cost of financing. While clean energy technologies have become more affordable, the capital required to deploy them remains significantly more expensive in many developing economies than in advanced markets. As a result, countries with some of the world’s best renewable energy resources still struggle to attract sufficient investment.

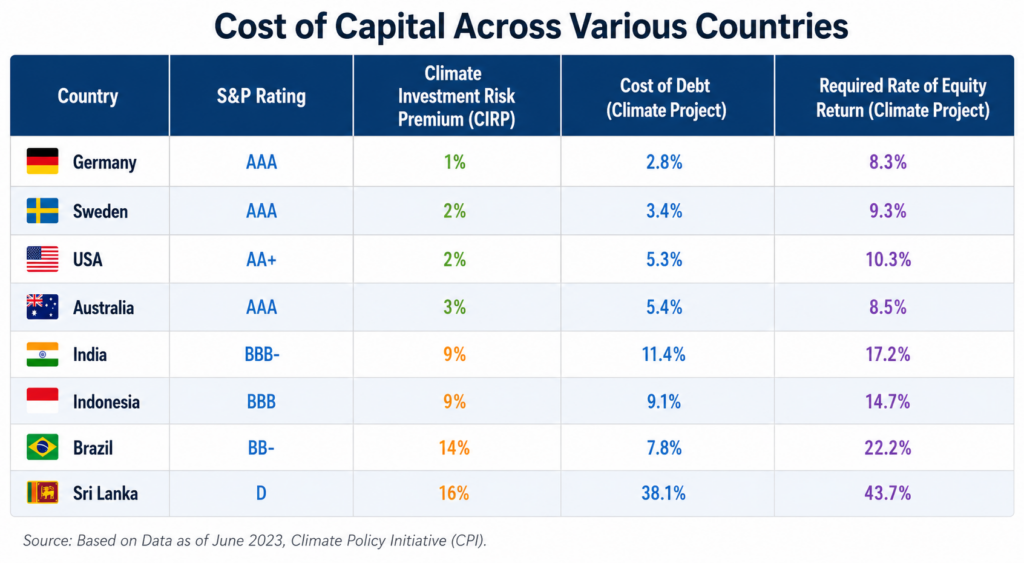

A renewable energy project in Germany can often secure financing at interest rates of 2% to 4%, while a comparable project in India may face rates closer to 9% to 11%. The technology is largely identical, and in many cases, developing countries have stronger solar and wind resources. Yet the economics of deployment diverge sharply due to differences in financing costs.

The Cost of Capital Divide

Renewable energy projects require substantial upfront investment but have relatively low operating costs over their lifetime. Unlike coal- or gas-fired power plants, which depend on continuous fuel purchases, solar and wind facilities generate electricity without ongoing fuel expenses.

As a result, the Weighted Average Cost of Capital (WACC)—a combination of the cost of debt and equity—plays a decisive role in determining project viability and the final cost of electricity.

The impact is significant. Analysis by the Global Solar Atlas shows that increasing a solar project’s WACC from 4% to 7% can raise electricity generation costs by roughly 40% to 50%, even when technology costs remain unchanged. In many cases, financing is as important as hardware in determining competitiveness.

The underlying reason is not technological, but financial risk perception. Developed economies such as Germany and France benefit from deep capital markets, stable currencies, strong institutions, and low sovereign risk, all of which reduce financing costs. Developing economies such as India and Brazil face higher sovereign risk premiums, currency volatility, inflation pressures, and smaller pools of long-term capital.

These factors explain why borrowing costs for renewable projects differ so sharply between markets, even when the underlying assets are identical.

Why Risk Matters More Than Technology

Investors evaluate far more than technology performance. They assess regulatory stability, currency risk, permitting timelines, land acquisition challenges, transmission infrastructure, and the creditworthiness of power purchasers. As these risks increase, the cost of capital rises.

According to Neha Khanna, associate director at the Carbon Policy Initiative (CPI), two key factors drive higher capital costs in many developing economies: sovereign and political risk, and foreign exchange risk. Speaking at a discussion hosted by Down To Earth, she noted that sovereign credit ratings directly shape investor expectations. “The lower your rating, the higher the premium that will be added,” she said.

In practice, this translates into higher risk premiums even when technologies and project fundamentals are the same.

Operational realities reinforce this gap. Developers in emerging markets often face delays in permitting, land acquisition, and grid connection. Transmission bottlenecks can delay commissioning and reduce expected revenues, while policy uncertainty weakens long-term investor confidence.

Macroeconomic conditions add further pressure. Higher inflation typically drives higher interest rates, increasing borrowing costs across the economy. Currency depreciation raises the cost of servicing foreign-denominated debt, while tighter global financial conditions can restrict access to long-term capital.

This challenge is especially important because experts predict that most future growth in energy demand will come from developing economies. Despite ambitious decarbonization targets across Asia, Africa, and Latin America, these regions also face the highest financing costs.

Decarbonization Needs Trillions, Not Billions

The financing gap is increasingly central to international climate negotiations, as developing economies argue that climate ambition must be matched by affordable capital.

At the June 2026 UN climate talks in Bonn, climate finance was once again one of the most contested issues between developed and developing countries. Many developing nations emphasized that climate targets cannot be achieved without lower-cost financing and greater access to capital.

India, for example, aims to reach 500 GW of non-fossil electricity capacity by 2030 and achieve net-zero emissions by 2070. This will require massive investment in renewable generation, storage, transmission networks, green hydrogen, electric mobility, and industrial decarbonization. But India’s challenge reflects a broader global financing gap.

According to analysis by the Global Renewables Alliance, renewable energy deployment will require around USD 8.6 trillion in investment between now and 2030. Of this, approximately 72% (USD 6.2 trillion) must come from debt, with the remaining 28% (USD 2.4 trillion) from equity.

Financing costs also shape investment in battery storage, transmission infrastructure, green hydrogen, EV charging networks, and industrial decarbonization technologies—all of which are highly capital-intensive.

This is where climate finance mechanisms become critical. Multilateral development banks, blended finance structures, credit guarantees, and currency risk mitigation tools can help reduce the cost of capital and unlock private investment at scale. Khanna highlighted one potential approach: a global guarantee mechanism backed by a supranational institution. This idea is reflected in CPI’s proposed Global Credit Guarantee Facility (GCGF), designed to reduce perceived credit risk and lower financing costs in emerging markets.

Ultimately, the central challenge is not the availability of clean energy technologies, but whether affordable capital can consistently reach the economies that need it most.